Renasant Corp. (NASDAQ: RNST) is a regional bank operating in Mississippi that is successfully taking advantage of both a unique resurgence in the state as well as in the American South. The bank holding company provides traditional banking services to the southeast, including industrial and commercial loans, residential mortgages, consumer deposits and wealth management services. The company recently closed the acquisition of KeyWorth Bank to expand its presence in Georgia and is looking to drastically enhance its wealth management footprint within the southern U.S. The real story, however, is two fold; the possibility that RNST is a proxy for an improving southern U.S. as well as RNST's ability to capture market share within its core divisions.

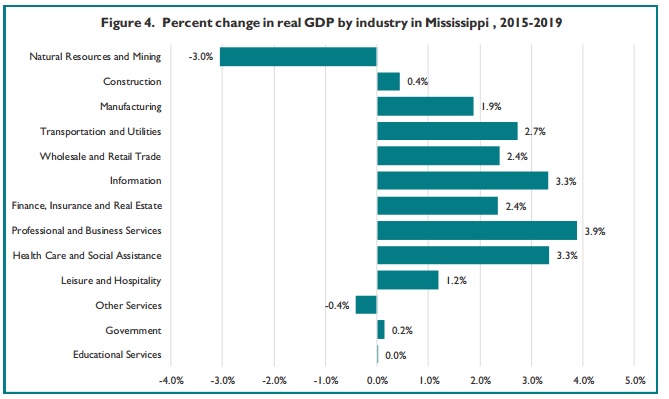

Mississippi has become a 'new economy' as traditional industries have given way to new markets within the state, creating a plethora of opportunity for business expansion (see Figure 1). Gone are the days of natural resource and government as the major drivers of employment and in are the days of new professional services, business services, health care and information. Moreover, unemployment in certain regions within the state are dropping to record lows while the annual percent change of incomes within the state is growing faster than the national level (see Figure 2).

Figure 1

Figure 2

Despite these macroeconomic catalysts, Renasant has been a prudent allocator of capital within the financial markets within which it operates as it has been able to appropriately capture revenue growth within its home state (see Figure 3). The company has a very healthy ROE near 8% while increasing book value per share by 25% over the last three years. Unlike other major diversified banks like GS, WFC, C or BAC, Renasant is trading at a slight premium (1.3 times book) which reflects the positive catalysts within the state in addition to southeast service expansion. Over the past 5 years, operating cash flow has more than doubled while operating income year-over-year has increased by 36.58%, which is very strong for a regional bank. Revenue growth over the last quarter has increased by over 47% and the 10 year average of revenue growth has surpassed 11%, which reflects the quality and prudence of management as it has been able to weather the financial crisis in a sustainable fashion. The more impressive metric, however, has been the bank's cash flow from sales which is at a remarkable 65.06%, which is almost double from last year. The reason why this is important is because this level of conversion allows the financial institution to have an abundant purse to continue its expansion within the southeastern U.S. while being able to take advantage of the economic turnaround happening within the state of Mississippi. In light of the bearish sentiment still present both with the U.S. and globally, it is impressive to see a financial institution with this kind of cash flow generation avoiding the typical excuses of a low interest rate environment we keep hearing from the bigger banks.

Figure 3

Figure 4

Source: finbox.io

There are certainly some headwinds facing the company, especially since RNST has performed so well and the market is starting to price in the southern U.S. region's improving economic picture. At 27.6x EV/LTM EBITDA, the company is not exorbitantly expensive (unlike peers HOMB and PNFP at 87.3x and 43.1x, respectively) but the company has compounded at over 20% per year for last 5 years and begging the question whether the ship has sailed. Moreover, just like any financial institution, the macroeconomic picture is a major variable bearing on future revenue and ROE growth and some are wondering whether we are starting to enter into peak unemployment and economic growth. However, there are reasons to believe this is not the case as U.S. GDP is expected to outpace Mississippi's growth.

Figure 5

Overall, we believe RNST below $30 creates a unique opportunity to participate in a growing regional bank in a very unique economic situation. Prudent and competent management, strong economic growth, low loan loss provisions, increasing cash flows and operating income combined with growing ROE (grew 6% from last quarter) should propel RNST towards becoming a financial institution worth north of $2 billion in market capitalization.