Good Morning,

More Fed watching this week. Yawn Yawn. U.S. stocks closed mixed on Friday, with utilities lagging, as investors digested remarks made by Federal Reserve Chair Janet Yellen and Vice Chairman Stanley Fischer.

The Dow Jones industrial average closed about 50 points lower after briefly falling more than 100 points. Earlier, Fischer told CNBC next week's jobs report would weigh on the Fed's rate hike decision.

Our take: The U.S. economy continues to show signs of recovery. Although we believe a rate hike is unlikely this year, if the U.S. continues to add jobs at a rate of more than 200,000 per month heading to year's end, we wouldn't be surprised to see the Fed raise rates by 50 basis points in December.

Something I’ve been thinking about a lot this week is the concept of “stopping”. These days we spend most of our time running around doing, scrambling to digest and process a seemingly endless flow of information. Are we able to come to a stop in our lives, even for one moment?

What stopping can do is make the going more vivid, more deep, more purposeful. Things get simpler. Meaningful information becomes more readily discernible as our inner voices become more present. By making time to “stop” every now and then, can we free ourselves to truly have time for the present and allow ourselves to be exactly as we are?

Thought of the Week

"If your mind isn’t clouded by unnecessary things, this is the best season of your life.” – Wu-Men

Stories and Ideas of Interest

- The Fed risks "shocking" consequences if it admitted outright that a hike wasn't coming this year, said Rabobank's Michael Every." It effectively would be locked into a paradigm where we can't ever really raise rates” an admission that monetary policy had become ineffective.

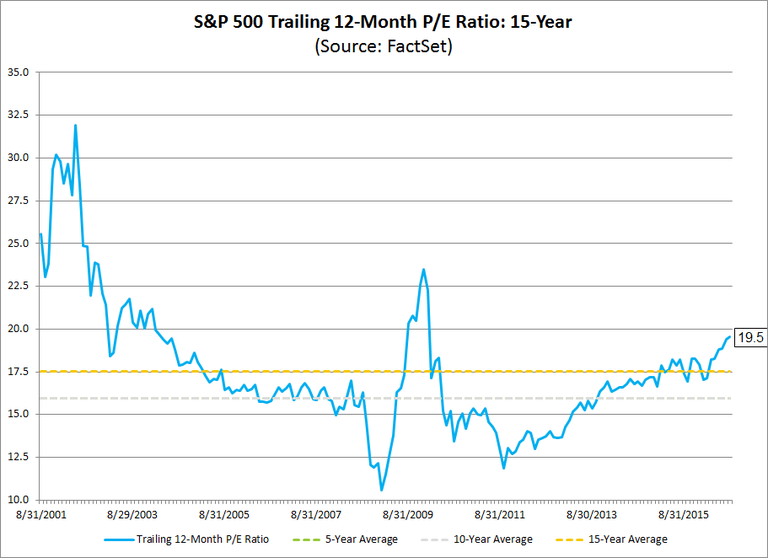

- More and more economic data points have erased the financial crisis and we appear to be quite close to where we started in 2007. The question is where is the risk? Has it disappeared? Or is it hiding somewhere investors haven’t looked yet?

Could emerging markets be an investment opportunity to consider? BlackRock said it upgraded EM equities to overweight as the firm expects a stable U.S. dollar, low rates and a better outlook for growth. Nevertheless, vulnerabilities remain. Indebted corporations in several emerging markets – including China and Brazil – could face trouble in the near future, which may send shocks reverberating through their national banking sectors. In addition, there is heightened risk of financial distress in the medium-term in Turkey.

- Could unaffordable housing prices be a good thing? Conor Sen for Bloomberg suggests that housing constraints in some cities in the U.S. accelerate economic development in emerging parts of the country. They decrease economic inequality between metro areas and lead to economic interdependence that drives civil rights. Quite interesting ideas to consider in light of Toronto's hot real estate market...

New housing crisis in the making? Prolonged low rates and dwindling liquidity for loans on the secondary market could grind home sales to a halt again…

- Could polls and betting odds be wildly inaccurate and Trump is going to be elected? Could people be lying about who they plan to vote for like they lie about what they are watching when they are being monitored? They won’t say it’s the Kardashians or Trump because it’s just too embarrassing… But when they are no longer being watched they may just go back to their favorite shows and their favorite politicians: those who offer the most mindless entertainment…4 years of Clinton in the Oval Office…who wants to watch that?

- Canada continues to be a hot asset class. Combined return from FX, bonds and stocks is highest since ’09 while Canadian economic data continue to disappoint. Will fundamentals eventually cool things off?

All the best for a productive week,

Logos LP