Good Morning,

The complacency and calm that characterized most of the summer is over! The tranquility that had enveloped global markets for more than two months was upended yesterday as central banks started to question the benefits of further monetary easing (ECB left things unchanged this week and some are suggesting that both Japan and Europe are going to start running out of bonds to buy…Governments may actually have to pick up the baton!), sending government debt, stocks and emerging-market assets to the biggest declines since June. The dollar also jumped and U.S. equities closed sharply lower as concerns the Federal Reserve might raise interest rates this month loomed following comments made by key Fed officials.

In addition, one of the most popular equity trades of the year broke down Friday as utility stocks and consumer staples shares tumbled as much as 3 percent while the yield on the 10-year Treasury note jumped. Thirty-day correlation between moves in the bond yield and the S&P 500 Index turned negative this month, meaning equity and Treasury prices are moving in the same direction. Attracted by high dividend payouts, investors have piled money into so-called defensive stocks this year as bond yields plunged.

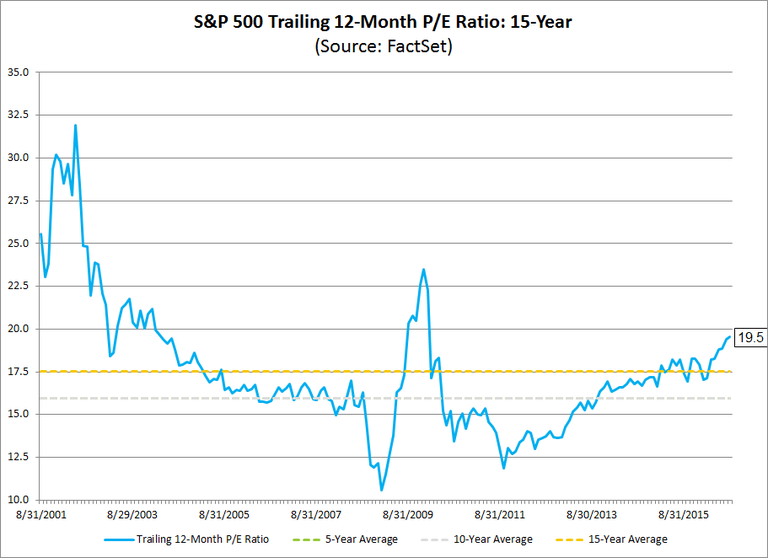

Time to take a hard look at your portfolio?

Our take: Firstly, this part of the year historically has 20-to-25 percent more volatility than any other time of the year. Secondly, Fed officials may be boxed into a corner where they have to raise rates in September in order to maintain credibility. They may not in which case markets will rally yet at this point, the balance is to the downside and thus it would be a good time to consider raising cash.

What to do? With interest rates so low for so long, and billions of dollars in government bonds around the world with negative yields, dividend stocks have been on fire. Yet with the probability of a rate rise increasing, these stocks are selling off….

Nevertheless, for the long-term investor they still may be your best bet. Long-term stock performance is helped greatly when companies not only pay dividends but reduce the share count by repurchasing shares.

Lower borrowing costs and a long economic expansion in the U.S. mean that domestic small- and mid-cap companies are in “great shape” as they’re holding a lot of cash.

Steven DeSanctis, an equity strategist at Jefferies used his bank’s data, as well as information provided by FactSet and Russell Investment Group, and calculated that, from the end of 1985, companies that reduced their share counts through buybacks while paying dividends outperformed the overall U.S. stock market significantly:

- Companies that reduced share counts achieved an average annual total return of 14.1%, compared with 6.7% for companies that let share counts rise or stay at the same level.

- Companies that paid dividends had an average annual return of 11.7%, versus 6% for non-payers.

- Companies that had done both — reducing share counts while paying dividends — had an average annual return of 13%, against an average return of 9% for the broader market.

If rate increase fears continue to drag the dividend payers down start looking for companies that have shareholder-friendly management (paying dividends and reducing share counts), healthy balance sheets, strong free cash flow and high ROIC.

Companies to consider: Cal-Maine Foods Inc. (NASDAQ: CALM), A&W Revenue Royalties Income Fund (TSE: AW.UN), Rocky Mountain Dealerships Inc. (TSE: RME), Grupo Aeroportuario dl Srst SAB CV (ADR) (NYSE: ASR), Brookfield Infrastructure Partners L.P. (TSE: BIP.UN), Enercare Inc. (TSE:ECI)

Thought of the Week

"New beginnings are often disguised as painful endings.” –Lao Tzu

Logos LP in the Media

Logos LP will be presenting at this year’s MoneyShow Toronto ConferenceSeptember 16-17, 2016 at the Metro Toronto Convention Centre. We will be presenting as a panel looking at family run businesses and whether the nature of their ownership can be an indicator of equity outperformance. Our Panel will be held at 2:45PM -3:30PM Sept. 17, 2016.

For more information on our talk please click here

There will be many other interesting speakers on both days so join us and Click here or call 800-970-4355 to register for your free spot at The MoneyShow Toronto! (please mention priority code 041782).

Our Head of Strategy opened the Toronto Stock Exchange last Friday with Big Brothers Big Sisters of Toronto as an Ambassador to the Financial Community. September is Big Brothers Big Sisters Toronto awareness month.

Stories and Ideas of Interest

- Does time kill periods of economic growth? Australia has now gone 25 years without being in recession, the second longest streak in the developed world. "But it is no time for complacency," said Treasurer Scott Morrison. "We continue to fight for every inch of growth." Official numbers from the Australian Bureau of Statistics revealed seasonally adjusted Q2 GDP growth of 0.5%, a shade under forecasts of a 0.6% increase.

- Wall Street’s next frontier is hacking into the emotions of traders. Startups wielding sensors and algorithms promise a new era of surveillance. Ben Waber, chief executive officer at Humanyze, discussesnew technology that measures and tracks traders' emotional responses in an attempt to limit losses and improve returns. He speaks on "Bloomberg Markets."

Conditions are right for a big city exodus. The stock market of the late 1990s is remembered mostly for high-flying dotcom equities that eventually crashed back to earth. Yet, from a money flows standpoint, the bigger imbalance of that era was that large-cap stocks fetched very high valuations relative to small cap stocks. This market opportunity was exploited by hedge funds, leading to a decade of outperformance and huge growth in the industry. Conor Sen for Bloomberg posits that in many ways, the national housing market is similarly positioned today.

- The World Wide Cage. Nicholas Carr for Aeon posits that technology offered to set us free. Instead it has trained us to withdraw from the world into distraction and dependency.

“What Silicon Valley sells and we buy is not transcendence but withdrawal. We flock to the virtual because the real demands too much of us..”

Has the internet given you greater sense of freedom in your life?

- An MIT scientist claims that he has invented a pill that is the fountain of youth. Leonard Guarente is certain he’s succeeded where doctors (and quacks) before him have failed. His pill will either extend lives or tarnish his career.

- Canada’s unemployment rate rose to 7% in August. Nearly half of all Canadians are draining their bank accounts between pay periods, and many are adding to their debt levels to cover expenses as they grapple with an uncertain economy, according to a poll released Wednesday.

- How do you raise a genius? The Scientific American presents the lessons from a 45-year study of uber smart children.

All the best for a productive week,

Logos LP

Disclosure: Logos LP is long Cal-Maine Foods Inc. (NASDAQ: CALM), A&W Revenue Royalties Income Fund (TSE: AW.UN), Rocky Mountain Dealerships Inc. (TSE: RME), Grupo Aeroportuario dl Srst SAB CV (ADR) (NYSE: ASR)