Good Morning,

U.S. equities closed at all-time highs on Friday, as the major indexes posted their best week since the election.

The Dow Jones industrial average rose about 130 points heading into the close, with 3M and Apple contributing the most gains.

All major indexes have been hitting record highs since the election. In fact, the Dow has notched 14 record closes since then and gains in 20 of the past 24 sessions.

Our Take

Although this rally is impressive, one should always pause and take the temperature of the market. Think of it as tying oneself to the mast as Odysseus did when the seductive Sirens attempted to lull his crew to destruction. What songs are the sirens singing now? What they seem to be chanting is a pro growth Trump administration. Is there logic to their songs?

Considering Trump’s potential to spend on infrastructure I read a great piece this week in Quartz which took a sober look at this hypothesis.

The author pointed out that markets are anticipating a big increase in spending and thus interest rates will begin to rise quite soon (they already have with news of a Trump victory as reflected by the yield on the 10 year). Higher interest rates will make all kinds of investment more expensive and can dampen growth. Meanwhile, the benefits of the infrastructure projects won’t appear for several years.

Thus, it seems how well Trump’s infrastructure plan will work will depend on how patient he is. Given the state of the economy, boosting economic growth will require picking useful infrastructure projects. These projects will have to have the potential to boost America’s productive capacity for years to come. As such, they might also leave a powerful legacy (imagine the Trump dam or Donald Trump bridge). But odds are those kinds of projects won’t confer much economic benefit, only cost, during his reign as president. And just how comfortable will Trump and his administration be with delayed gratification? How comfortable will the struggling white working class be?

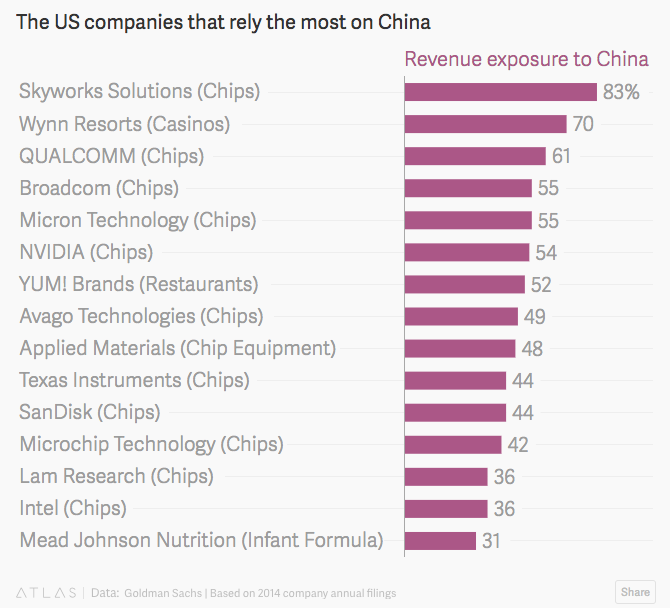

In fact, U.S. President-elect Donald Trump’s future policy stance poses “the single largest risk to the global economy,” according to a client survey by forecasting firm Oxford Economics Ltd. More than half of respondents said that the probability of a sharp slowdown has increased over the past three months, according to the firm’s Nov. 14-21 survey on global risk perceptions conducted among about 180 clients and contacts. The main fear is a potential trade war with China.

What would this even look like? Interesting article in Quartz highlighting which US companies would suffer most if a trade war broke out:

Based on some these concerns should we be skeptical of the “Trump Rally”? Well the same study above also sited Trump as the most likely source of faster global growth, with 38 percent citing the potential for the U.S. economy to surge on new fiscal stimulus he has proposed…Does anyone know anything? If things do improve look to increase exposure to small caps as they will benefit the most from potential regulatory reforms.

Interestingly another view can also be argued. Although the Trump phenomenon can be viewed as a lesson in the laws of power, it can also be viewed as a challenge to traditional economics. Mark Buchanan for Bloomberg argues that although Trump’s move to bully companies into keeping jobs in the U.S. can be viewed as foolish or populist, they do raise some important questions about how we should define economic success.

Significant changes are often preceded by small actions. Could Trump’s "nativist' actions be construed as a promotion of a new set of values? The current economic view - that it is acceptable for businesses to move manufacturing jobs to areas where profitability and competitiveness can be enhanced - may simply be outdated….

Have Trump voters hinted that companies should have a different set of values? Perhaps an allegiance to their communities and employees? Given the stagnant economic position the vast majority of people find themselves in, how strange is it to suggest that economic purism may have lost its shine?

Either way the Shiller CAPE market valuation ratio is now over 27, which is near the level we saw before the market crashes in 1929, 2000, 2008… Two decades after then-Federal Reserve Chairman Alan Greenspan fretted about asset prices reaching unsustainable levels -- a pronouncement that caused a brief interruption in the U.S. stock rally -- his successors might be tempted to warn again markets are getting ahead of themselves...

Funnily enough the latest figures from FactSet, a financial-data provider, show that 49% of firms in the S&P 500 index of leading companies are currently rated as “buy”, 45% are rated as “hold”, and just 6% are rated as “sell”. In the past year, 30% of S&P 500 companies yielded negative returns. Keep calm and compound on....LOL

Expect the rally to continue at least into the new year as 90%+ of hedge fundsare trailing their benchmarks and will look to play catch up yet remember that bull markets die of euphoria not pessimism.

Thought of the Week

"MASTER THE ART OF TIMING - Never seem to be in a hurry- hurrying betrays a lack of control over yourself, and over time. Always seem patient, as if you know that everything will come to you eventually. Become a detective of the right moment; sniff out the spirit of the times; the trends that will carry you to power." -Robert Greene

Stories and Ideas of Interest

What risks does the global economy face in 2017? Apart from Donald Trump’s administration as outlined above Nomura has come out with a list of grey swans (“These are the unlikely but impactful events that, in our opinion, lie outside the usual base case and risk scenarios of the analyst community”).

Potential shock 1: U.S. productivity might boom

Potential shock 2: China might float its currency

Potential shock 3: The European Union (EU) could reform, leading the U.K. to re-join

Potential shock 4: Japan inflation might surge

Potential shock 5: The U.S. Federal Reserve could be muzzled

Potential shock 6: Russia may flex its muscles

Potential shock 7: A clearing house may fail

Potential shock 8: Japan Prime Minister Shinzo Abe loses power

Potential shock 9: Emerging market capital controls may return

Potential shock 10: Paper money may disappear

- It is too early to say the era of low yields is over. The Economist explores how the market has begun pricing in three factors which are usually drivers of higher bond yields —faster growth, rising short-term rates and higher inflation. Nevertheless, this bond-market sell-off needs to be set in context. During the “taper tantrum” of 2013, when the Fed signalled a slowing of its quantitative-easing programme, the ten-year yield reached 3%. It was as high as 2.47% in June last year. Furthermore, it is not clear how much of Mr Trump’s programme will be implemented, nor indeed whether economic growth or inflation will actually rebound. In addition, a rise in bond yields may play a part in choking off economic growth. The ratio of total debt (governments and private sector combined) to GDP has risen in both developed and developing economies since the 2008 crisis. “A large stock of debt needs a low interest rate to make it tolerable.

- Do you make less than an entry level employee in Silicon Valley?Competition for engineering talent remains fierce in Silicon Valley. The megaplayers offer recruits lavish offices and gourmet cafeterias along with all the usual corporate perks, such as gym memberships and expense accounts. But there's nothing like good, old-fashioned money to entice top talent. An unscientific survey in Bloomberg tries to put a price on some of the hottest jobs in tech.

- Some of the apparent income mobility in places like Canada or Scandinavia is something of an illusion. Income mobility is a problem for everyone. Most people, in most countries, dream of a world where birth does not limit your status in society. No country has achieved this happy end, though some of them do better than others. Income mobility statistics are created, worried over, analyzed for some sign of possible cures. A new paper out of Sweden suggests that we should perhaps be worrying even more than we do, and that the cures may be harder to come by than we thought. What is interesting here is that if family history is such a major component of financial success then this weakens some of the evidence for supposed present day discrimination…Is redistribution the only way???

- Upset with your government and feeling disillusioned? Move to a seastead. Imagine, for instance, autonomously governed sea platforms, with a limited number of citizens selling health and financial services to the rest of the world. Advances in robotics and artificial intelligence might make the construction and settlement of such institutions more practical than it seemed 15 years ago. Technocratic utopianism or path to greater human companionship?

All the best for a productive week,

Logos LP